What the OECD’s latest data tells us about global aid in 2022

The Organisation for Economic Co-operation and Development’s Development Assistance Committee (DAC) recently published its final aid data for 2022, and it’s not good news for the world’s least-developed (LDCs) and low-income countries (LICs).

Their share of total Official Development Assistance (ODA) fell to its lowest level since 1996, while growing debt and increasing interest rates added to a challenging economic picture. Most attention will understandably be on unprecedented in-donor refugee costs, and support for Ukraine bringing headline ODA to new highs, but that’s not the whole story.

This blog also explores other important trends which risk getting lost among all the focus on records being broken as a result of the invasion of Ukraine. For a more systematic look at what the new data says, see Development Initiatives’ new factsheet.

Aid to Ukraine breaks ODA records

Total aid disbursements from DAC members and multilaterals was $269 billion in 2022: a 24% increase relative to 2021, and a remarkable 40% increase relative to 2019 (in constant prices). However, when aid to Ukraine, in-donor refugee costs (which increased by almost 150% in 2022) and COVID related aid are removed, the increase, compared to 2019, falls to a more modest 2%.

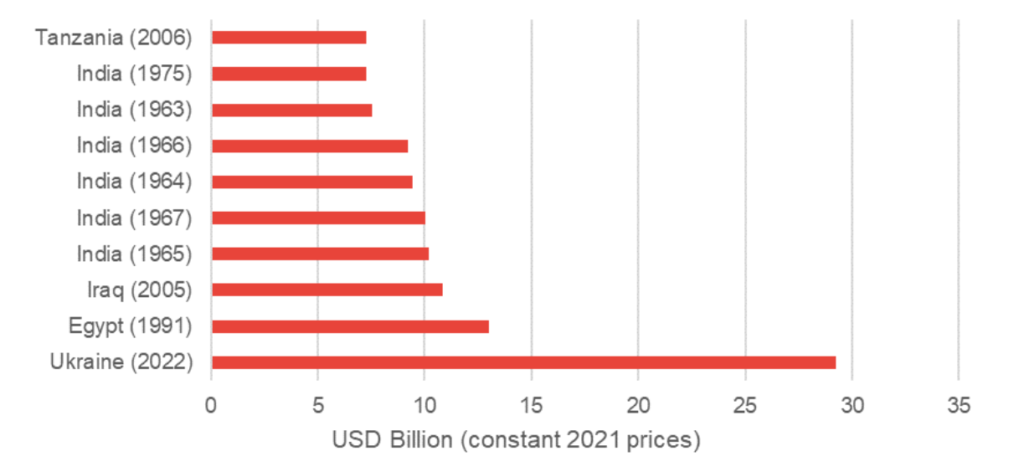

Fig 1: Top 10 largest amounts of aid received in any one year (excl. debt relief)

As anticipated, Ukraine was the country to receive the most ODA in 2022 by a wide margin, as countries and multilaterals scrambled to support Ukraine following Russia’s invasion. At $29 billion, Ukraine received more aid than any country has ever received in one year from DAC members and multilaterals.

The next largest was Iraq in 2005 ($27 billion in 2021 prices) but that was only because of a huge amount of debt relief on export credits that many argue should not have counted as ODA. Excluding debt relief (figure 1), Ukraine received more than double the amount of the second largest recipient in any single year, Egypt, which received $13 billion in 1991.

It is obviously right that DAC members and multilaterals acted swiftly to support Ukrainians. But the rapid scale up in development finance (let alone military and other forms of assistance) might raise eyebrows in the context of a lacklustre response to COVID-19, continued failure to meet targets for climate finance or spending in LDCs, and the paltry pledges to the new loss and damage fund.

LDCs received less aid, and less in grants

When aid spent in provider countries is removed, ODA disbursements to LDCs and other LICs (henceforth LDCs) were 3% lower in 2022 than in 2021. This is partly a result of support for COVID-19 control falling from its peak, but it also reflects a longer term trend. Excluding COVID support, cross-border aid* to LDCs has been stagnant for around six years: in 2022, it was roughly $57 billion, broadly unchanged relative to 2017.

In addition, LDCs have been receiving more aid as loans instead of grants in recent years, and this continued into 2022, which meant that grant financing fell even faster than total aid. Between 2021 and 2022, grants to LDCs fell by 5%, and, excluding COVID-19 support, grants to LDCs fell by 11% between 2017 and 2022. This is a drop from $44 billion to $39 billion, the lowest level since 2014 (in constant prices).

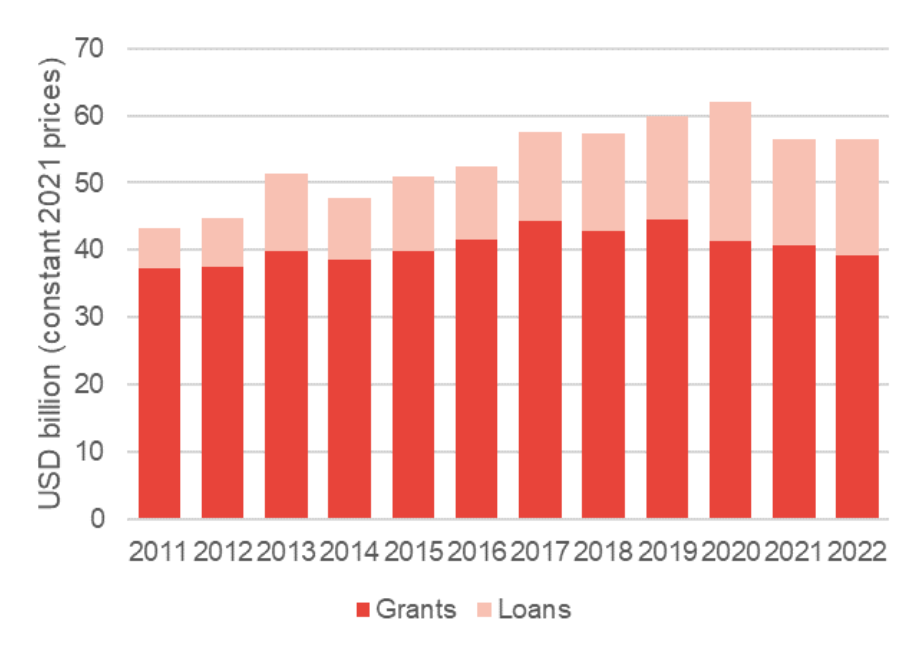

Fig 2: ODA disbursements to LDCs, excl. In-provider aid and COVID-19 support

This trend is partly because the composition of LDC financing has changed. Multilaterals now account for 47% of ODA disbursements to LDCs, up from 35% in 2011, and are more likely to provide ODA in the form of loans.

But DAC aid is also shifting towards loans. This share was 16% in 2022, up from 12% in 2021, and from 4% in 2012, which was the year in which the DAC began the process of updating how loans are counted as ODA (I’ve argued elsewhere that the rules risk incentivising loans over grants). Excluding in-provider ODA, grants from the DAC to LDCs have been essentially stagnant for around a decade. If COVID costs are also excluded, they are now below 2010 levels.

This is despite increasing concerns about the level of debt held by LDCs, ten of which are already deemed to be in debt distress by the IMF, with another 26 at high risk. Since 2011, external debt owed by LDC governments has increased by $200 billion, from $144 billion to $344 billion. Around half of this is due to an increase in debt owed to multilaterals and ODA loans from DAC members.

Loans are becoming more expensive

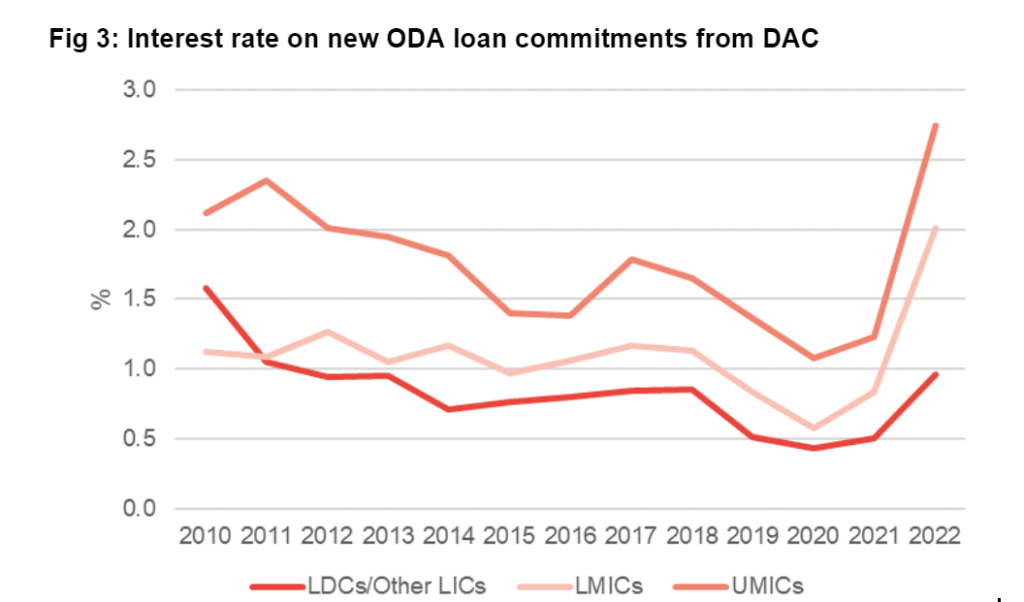

As the use of loans has increased (for all income groups), they have also become more expensive. The average interest rate charged on new loan commitments from DAC members in 2022 increased substantially, from 0.9% to 2.0%, and as figure 3 shows, this was felt across income groups.

Fig 3: Interest rate on new ODA loan commitments from DAC

This is not surprising. Interest rates in many creditor countries rose substantially in 2022 as central banks fought to control inflation, and many aid loans are directly linked to these interest rates. Furthermore, it meant that the cost of government borrowing rose in creditor countries, and in 2022 these cost increases were ‘passed on’ to developing countries in the form of more expensive loans.

The immediate impact of these rises will be moderate. Loan commitments tend to take years to be disbursed, and therefore the higher rates of these loans will not be felt for some time. Nevertheless, given the burgeoning debt crisis, any additional cost of borrowing is unwelcome.

Declining concessionality for those who need it most

The Russian invasion of Ukraine made 2022 a highly unusual year for ODA. In-donor refugee costs were high enough that several countries started to question whether it should all count, and Ukraine became the best funded humanitarian situation by some margin, more than doubling the record for the most aid received in one year by any country. And this followed two years in which extraordinary measures taken to control COVID (and controversial rules) made overall aid trends hard to discern.

However, one clear trend is that ODA is becoming less concessional, as countries move further away from grant financing, and loans become more expensive. This is a trend that should concern those interested in promoting development.

It is vital that in 2024, greater priority is given to those in the least-developed countries who risk being left behind.

Read the European network on debt and development, Eurodad’s reaction to 2022 OECD DAC figures

* Throughout this section the data refers to cross-border aid, and so excludes in-donor refugee costs, in-donor student costs, promotion of development awareness, administrative costs and debt relief.

Category

News & Views